{kind=link}

A degree from a prestigious university in the US, UK, Canada, or Australia is often seen as a ticket to international careers, better salaries, and wider opportunities. However, this dream comes with a rapidly escalating cost, which can easily run into crores.

For many Indian parents today, preparing for their children’s foreign education has become as important as buying a house or building a retirement corpus.

But most families underestimate the true cost. They calculate tuition fees, but often forget accommodation, health insurance, travel, visa expenses, not to mention currency fluctuations, and rising education inflation. By the time the actual bills start coming in, the financial burden can become overwhelming.

Experts say this is exactly why planning early matters and explain the best way to fund your children’s dream.

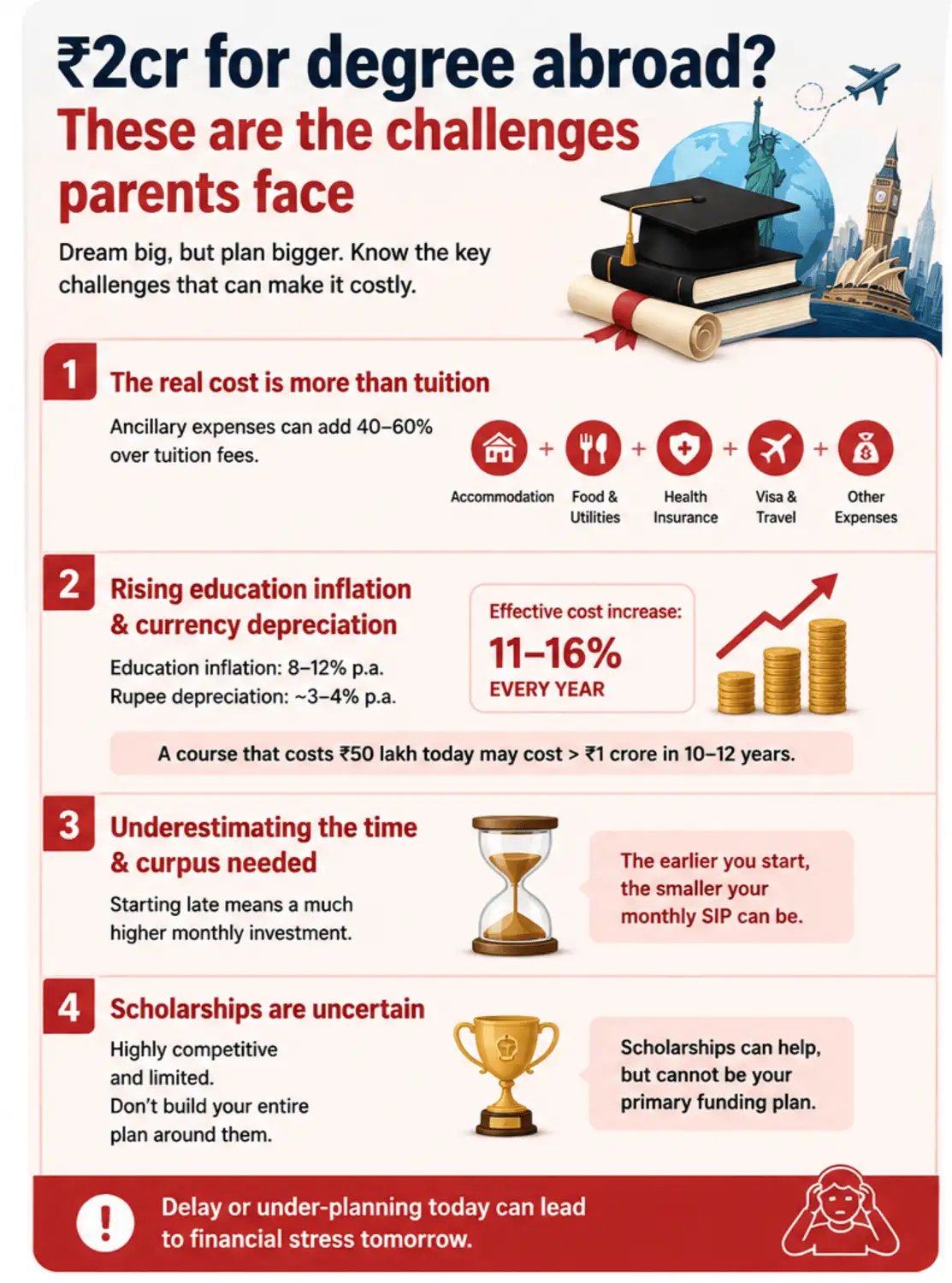

Costs beyond tuition: What other expenses parents must think of

A common mistake parents make while planning for overseas education is focusing only on tuition fees.

But tuition is only one part of the total expense.

Ancillary expenses such as accommodation, food, utilities, health insurance, visa fees, and travel can push up the total cost by another 40–60% above tuition fees alone, according to Swati Jain, CEO Wealth, Arihant Capital Markets.

“In countries like the US, UK, Canada, and Australia, undergraduate programmes can range anywhere between $25,000 and $60,000 per year, and that’s before adding living expenses, which can easily be another $10,000 to $20,000 annually,” says Sonal Kapoor, Global Chief Business Officer, Prodigy Finance.

Over a span of three- or four-years, the total cost can really add up for most middle-class families.

This is one reason why a lot of families are now starting to reconsider their strategies for planning overseas education, says Kapoor.

She explains that completing undergraduate studies in India and pursuing a postgraduate degree abroad prove to be a more financially sustainable route.

Postgraduate programmes are typically shorter, usually one or two years, and more closely linked to career outcomes. Tuition fees for many master’s programmes range between $30,000 and $70,000 in total, excluding living costs, according to Kapoor.

While that’s still expensive, the shorter duration reduces the financial burden significantly.

ET Online

ET Online

These are the challenges parents face while planning for their children’s foreign education

Also Read: A foreign degree at zero cost? These scholarship strategies can turn your dream of overseas education into fully funded study

Education inflation: One of the biggest risks parents ignore

The cost of foreign education is not just high, it is rising rapidly every year.

Education inflation globally is estimated at around 8–12% annually. At the same time, historically, the Indian rupee has depreciated by about 3–4% annually against major currencies such as the US dollar over the last 15 years, according to Jain.

Taken together, this means the effective increase in overseas education costs can be as high as 11–16% every year.

This has a huge impact on long-term planning.

A course that costs ₹50 lakh today may easily cost more than ₹1 crore after 10–12 years due to inflation and currency depreciation alone.

A lot of families tend to plan according to today’s costs without considering future inflation. This can really catch the parents off guard, when the time arrives, adds Jain.

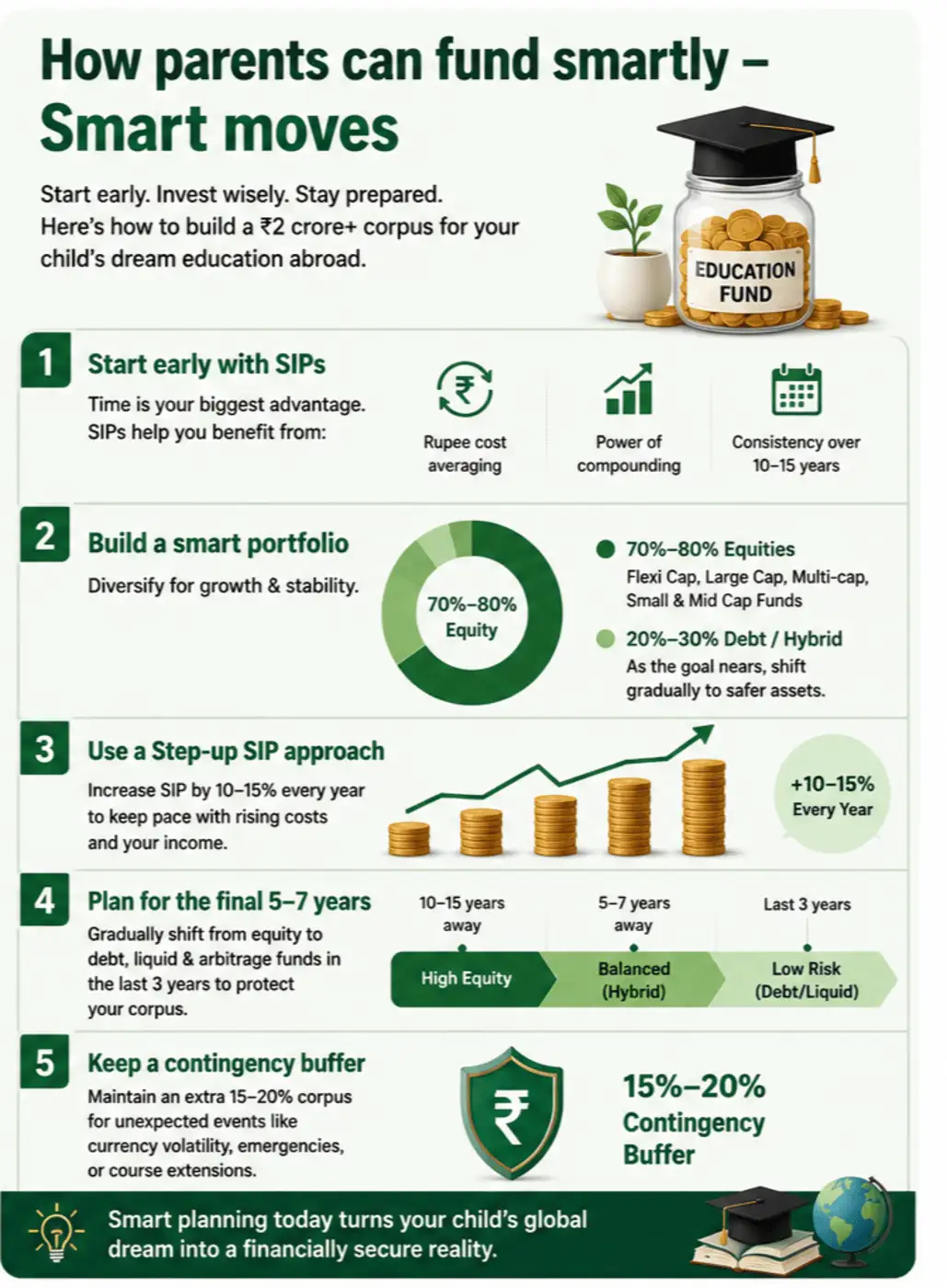

She also advises building a contingency buffer of at least 15–20% to handle unexpected expenses such as emergency travel, currency volatility, or course extensions.

How to start investing for your child’s foreign education fund

This is because long-term investing gives money time to compound.

A parent who starts investing when the child is five years old, has over a decade to build a corpus before undergraduate education begins. That long time horizon allows even moderate monthly investments to grow meaningfully.

Experts say SIPs remain one of the most effective tools for this goal.

This investment strategy encourages consistency, benefits from rupee cost averaging and if started early, provides an added advantage of compounding over a 10–15-year horizon ensuring a steady wealth creation over time, according to Jain.

“A child’s SIP portfolio should be well diversified including flexi cap, large cap funds and multi-cap funds, as core allocation for stability, paired with small & mid cap funds for growth and higher returns,” she suggests.

Equally important is increasing investments gradually over time.

She advises parents to adopt a “step-up SIP” strategy, increasing SIP contributions by 10–15% annually to keep pace with rising education costs and income growth

For instance, if you are targeting a corpus of Rs 3 crore after 15 years and expect a return of 12% from equity MF then you need to have monthly SIP of Rs 63,100.

Normal SIPs

| Time Horizon | Starting Monthly SIP | Total Amount Invested | Final Corpus |

| 10 Years | 1,34,000/month | ₹ 1,60,80,000 | ₹ 3,00,20,809 |

| 15 Years | 63,100/month | ₹ 1,13,58,000 | ₹ 3,00,31,271 |

| 20 Years | 32,700/month | ₹ 78,48,000 | ₹ 3,00,79,336 |

However, if you go for step-up SIP you can start with lower monthly investment in first year as 48,500 but increase it annually by 5%.

Step-up SIPs

| Time Horizon | Starting Monthly SIP | Annual SIP Step-Up | Total Amount Invested | Final Corpus |

| 10 Years | 1,11,500/month | 5% | ₹ 1,68,29,220 | ₹ 3,00,34,157 |

| 15 Years | 48,500/month | 5% | ₹ 1,25,58,724 | ₹ 3,00,26,789 |

| 20 Years | 23,600/month | 5% | ₹ 93,64,278 | ₹ 3,00,98,786 |

ET Online

ET Online

Smart moves parents can make to fund their children’s foreign eduaction

Also Read: Can you fulfil your study abroad dream without going broke? Here are 7 ways to minimise costs

How much equity exposure is enough for your children’s education portfolio?

In the early years, when the goal is still 10–15 years away, parents can afford to take a higher equity exposure because they have time to ride out market volatility.

Maintain 70–80% allocation towards equities during this phase, recommends Jain.

But as the child approaches college age, the investment strategy should gradually become more conservative.

Five to seven years before the goal, parents should start shifting part of the portfolio towards hybrid funds and safer assets.

In the final three years, the focus should move towards debt, liquid, and arbitrage funds to protect accumulated gains from market shocks.

Should parents depend on scholarships?

Many families hope scholarships will reduce the financial burden substantially.

While scholarships can certainly help, experts caution against building an entire financial plan around them.

Scholarships are highly competitive and global in nature, meaning even academically strong students may not secure one, says Kapoor.

This is why she advises families to separate “guaranteed” funding from “uncertain” funding.

In practical terms, parents should first plan using family savings, investments, education loans and treat scholarships as an additional benefit rather than a certainty.

“Families should ideally start preparing for scholarships at least 12 to 18 months in advance. A lot of strong scholarships open early, and the process itself takes time, from writing essays to getting recommendations right,” she says.

Assistantships can also help, especially for postgraduate students. Research or teaching assistantships often support living expenses and reduce financial pressure during the course.

Education loans are no longer a last resort

In India, education loans were once viewed as something families used only when they lacked savings. Today families are increasingly using education loans rather than exhausting their life savings.

“On a broader level, many students globally adopt a balanced approach, combining family support with loans and scholarships,” says Kapoor.

Education loans for foreign studies are designed to cover the total cost of attendance, including tuition and living expenses, says Kapoor.

Most loans provide a grace period after graduation, allowing students time to secure employment before repayments begin.

Tax benefits are available under Section 80E of the Income Tax Act, where interest paid on education loans qualifies for deduction for up to eight years under the old income tax regime.

Still, experts caution families against excessive borrowing. The repayment burden should remain manageable relative to expected post-study income.

The dream of studying abroad is becoming increasingly common among Indian students. But so is the financial pressure that comes with it. The good news is that early planning can make a massive difference.