For the well-heeled investor, there is never a dearth of options. If you have a meaty portfolio, an asset manager or wealth advisory platform will offer ‘tailored’ solutions. Those seeking exclusivity often flirted with equity portfolio management services (PMS). However, the PMS space was not catering to individuals sitting on a hefty mutual fund (MF) portfolio— most were flying solo and rudderless.

Enter PMS for MFs, where fund selection, advice and execution come embedded. Wealth-tech platforms and private wealth firms are increasingly pitching “curated MF portfolios” with active allocation, tactical shifts and personalised advice. Are MFs in a PMS wrapper solving a genuine gap? Can they deliver enough bang for the extra buck?

The MF-PMS sales pitch

When investing in MFs, investors face problem of

- Choice of 2,500+ schemes

- Product pushing rather than holistic allocation

- Generic model portfolios

- Lack of personalisation

- Excessive scheme clutter

- Behavioral gaps-panic selling, return chasing

PMS-style MF advisory attempts to offer

- Customized asset allocation

- Curated fund selection

- Tactical shifts based on market conditions

- Goal-based portfolio construction

- Continuous rebalancing and monitoring

- Consolidated reporting and handholding

- Seamless execution

How it differs from RIA

- RIA can’t exercise discretionary control over client assets

- Leaves execution and implementation to the client

- MF-PMS removes friction, improves timely execution

- Fund switches may happen dynamically

A marriage of convenience

In essence, an MF-PMS creates personalised fund portfolios for affluent clients. It is aimed at combining the simplicity and tax-efficiency of MFs within a professional advisory structure. The sales pitch says that with over 2,500 MF schemes in India, investors face a problem of plenty. MF-PMS providers claim they use institutionalgrade research to pick the best funds.

Apart from having to choose funds, behavioural discipline remains a handicap. Investors often pursue ‘alpha’— or outperformance—in MFs, but experience a return drag over time, fetching returns lower than those of their chosen funds. This is a behavioural gap—investors panic, make emotional switches or chase hot performers, diluting returns.

ALSO READ | The true cost of PMS returns: Disclosing the hidden gap between headline numbers and real investor gains

The MF-PMS aims to improve longterm outcomes through disciplined allocation and risk management rather than mere fund selection. This is the real alpha that they seek to deliver. To solve this problem, they charge a fee.

Sandeep Jethwani, Co-founder of wealth management firm Dezerv, observes that 53% of MF investors’ portfolios underperform their benchmarks, and only 1% beat them by more than 1%. “Good funds exist. Selecting them, maintaining the right asset allocation, customising it to specific goals and liabilities, monitoring holdings scattered across platforms, and resisting behavioural traps like chasing past performance or novelty bias is hard work. Most investors do not have the time, the data or the temperament to do this consistently over a decade or more. That is what the PMS fee pays for.”

Not everyone is convinced that PMS in MF offers any distinct value proposition compared to what a registered investment advisor (RIA) already does. Dhirendra Kumar, CEO of investment research company Value Research, says, “Selection and allocation are solvable by any competent RIA on a flat fee. The PMS wrapper is chosen because it permits performance fees, not because the investor needs it.”

Others argue that while both appear similar on the surface, the depth of engagement can differ meaningfully. This is because an RIA typically cannot exercise discretionary control over client assets the way a PMS can. While RIAs can advise clients what to do, PMS structures can actually manage and execute within agreed mandates.

According to Vidya Bala, Head— Research at portfolio management firm PrimeInvestor.in, “For a MF-based PMS, the management fee covers active portfolio construction across multiple funds and asset classes, tactical rebalancing based on market conditions, staggered deployment based on valuations, and 100% in-house research-driven decision-making—none of which an investor can replicate passively or a typical RIA can deliver in the same structured manner.”

She says RIAs, by their very structure, advise— but don’t actively manage. Execution remains with the investor and responding actively to changing market and category conditions is cumbersome within the RIA framework, Bala adds.

Srikanth Bhagavat, Managing Director and Principal Advisor at Hexagon Capital Advisors, concurs, “As an RIA, it is difficult to get all clients to agree on suggested actions in a time-bound manner to enable timely execution of advice. This is a challenge when there are hundreds of portfolios to administer the advice to.”

ALSO READ | Too many smart beta funds? Here’s how investors can cut through the passive investing noise

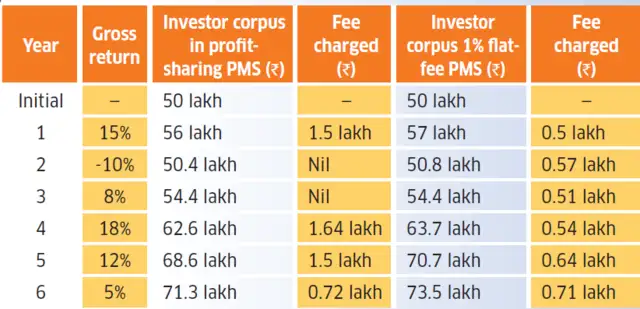

Profit-sharing PMS vs flat-fee PMS

How MF-PMS offerings have fared During strong bull markets, a flat-fee structure may leave more upside for investors because the fee is capped.

Assumptions: Initial investment: Rs.50 lakh. Profit-sharing PMS fee: 20% of annual gains. Flat-fee PMS charge: 1% of opening assets under management annually. Returns before fees are identical for both PMS structures.

How MF-PMS offerings have fared

Source: PMS Bazaar, Securities and Exhange Board of India. Benchmark return pertains to index chosen by the PMS strategy. The above list is not exhaustive. Returns as on 30 April 2026; returns over a 1-year period are annualised; returns are calculated using the time weighted rate of return (TWRR) method and as provided by the respective AMCs.

Seeing double?

Critics suggest the ‘double-dip’ fee structure of MF-PMS makes the product unfavourable. Investors pay the PMS management fee in addition to the expense ratios of the underlying MFs. “A typical MF-PMS charges 0.6–1% fixed, or a 20% profit share, and that sits on top of the underlying scheme’s expense ratio (0.5–1% in direct plans). The all-in cost ranges from 1.1–2% for the same job,” explains Kumar.

A MF manager and a PMS manager are not doing the same job, and the different fees are not paying for the same work, Jethwani insists. “The MF’s expense ratio pays for what happens inside the fund: research, security selection, and execution within a defined mandate. The PMS fee covers customised portfolio management, asset allocation as per financial goals, selection of right funds, execution of trades, and the behavioural layer that keeps the portfolio on plan through cycles.”

Bala says the “dual fee” framing is misleading, arguing that every managed investment structure involves a service fee of some kind. A distributor earns a commission on top of the regular plan’s expense ratio. An RIA charges an advisory fee in addition to direct plan expense ratios. Similarly, a PMS charges a management fee. “There is no fee-free professional management—the question is only about what you get in return,” she remarks.

Profit sharing vs flat fee

The viability of MF-PMS varies based on how it charges the management fee. Some charge a fixed fee while others adopt a profit-sharing model. Under the flat fee structure, investors pay a fixed percentage of assets under advice, usually up to 1%. In profit-sharing, the PMS charges a certain percentage on gains and follows the high-watermark principle.

ALSO READ | ‘Most Indians retire asset-rich but income poor’: Edelweiss MF’s Radhika Gupta on retirement planning, SIP resilience, lifecycle funds, and simple investing

In other words, a PMS manager earns a performance fee only on incremental gains at every interval. This ensures that investors don’t pay fees twice on the same gains or to recover losses.

So, a portfolio that initially grows from Rs.50 lakh to Rs.55 lakh can be charged a fee on the incremental gain. However, if its value falls to Rs.52 lakh the next year, and Rs.54 lakh the year after that, fee can’t be charged for both years. Some include a hurdle rate— a minimum gain before a manager can share the profits.

PMS providers often tout this profit-sharing model as more investor-aligned. Kumar suggests this alignment does not hold up to scrutiny. “The performance-fee structure is asymmetric. These strategies pay the manager handsomely when markets rise. The same hurt only the client when markets fall. That is heads I win, tails you lose, dressed up as alignment.”

Some new-age MF-PMS offerings have no hurdle rate at all, which means the manager earns a performance fee simply for delivering what an index fund gives the investor for free. A flat fee, on the other hand, aligns the adviser with the investor’s lifetime relationship, not with this quarter’s trade. “Once you strip the marketing, performance fee is a feature for the manager; flat fee is a feature for the investor,” Kumar explains.

Rajani Tandale, Senior Vice President—Mutual Fund at 1 Finance, points out, “Independent analysis shows performance-fee structures can cost investors 2–3 times a flat-fee arrangement in strong market years. Profitsharing has merit only where the manager has a verified, benchmark- relative alpha edge across full market cycles.”

Many MF-PMS providers agree that the flat fee is the superior model. Dezerv offers both structures, but Jethwani recommends the flat fee model for its predictability. “The cost and the manager’s incentive remain consistent across cycles, unlike the profit share model where the fees can be lumpy during market rallies and absent during flat or bear markets.”

PrimeInvestor only charges a flat fee. Bala explains, “Profit sharing can often create perverse incentives: the manager is tempted to take outsized risks or churn the portfolio to generate short-term gains that trigger taxes and churn costs. It also penalises investors in good years by taking a pound of what belongs to them.”

She also maintains that the flat-fee structure does not always favour the RIA model. “As portfolios grow, the fee differential at a flat-fee PMS narrows further in the investor’s favour. The assumption that RIAs are automatically cheaper does not hold at the HNI (high-net-worth investor) scale,” according to Bala.

Active vs passive

The viability of MF-PMS is further complicated by the choice of underlying funds—active or passive. It makes the cost argument sharper, says Kumar, adding, “If the underlying is active, the investor is paying for active management twice, once to the asset management company (AMC) and once to the wrapper, with no evidence that two layers of judgment beat one. If the underlying is passive, the wrapper is charging an active fee for asset allocation.”

When the PMS deploys into low-cost index funds and exchange-traded funds (ETFs), the combined cost—advisory fee plus fund expense—stays in the 0.6–1.2% range, which is competitive. But stack that same advisory fee on top of actively managed funds that already charge 1.5–2.5%, and the total annual drag climbs to 2.5–4%, suggests Tandale. At that level, the underlying funds don’t just need to beat the market, but beat it by enough to justify each basis point of that combined cost. That is a steep bar to clear.

As Tandale puts it, “Stack the same advisory fee on actively managed funds, and the combined drag demands consistent, verifiable alpha—a high bar given that a significant majority of active funds have historically underperformed their benchmarks.”

Bala counters that even if the embedded expense ratio is higher in active fundsbased PMS, the combination of superior fund selection, timely category rotation, and disciplined position-sizing can more than offset the management fee. Jethwani maintains the structural case for MF-PMS does not change whether the underlying is active or passive, because the work above the fund has to be done regardless of how the underlying is constructed.

Churn, baby, churn

Critics argue this is where the fee math can really unravel for an MF-PMS. In regular MFs, a fund manager can rebalance the portfolio within the scheme without triggering a tax event for the investor. Tax is paid only when the investor redeems. That deferral compounds.

“A PMS does not enjoy that,” insists Kumar, adding, “Every trade the manager places is in the investor’s own demat account. Every realised gain is the investor’s taxable event in the year it occurs.” He reckons that a high-churn PMS has to clear a meaningful tax drag before it can claim alpha against a buy-and-hold mutual fund portfolio.

“The erosion scales with turnover,” stresses Tandale. “Depending on churn frequency, a PMS-on-MF strategy needs to generate in excess of 2-3 percentage points of additional gross returns annually just to match the post-tax outcome of a buy-and-hold MF approach.”

But service providers counter this argument. Jethwani says any sale of MF, whether by the clients themselves with advice from an RIA or in a PMS by its manager, receives the same tax treatment. Even when the MF-PMS must churn, it does so modestly. “At Dezerv, we don’t churn for the sake of churning unless we believe there is a really good opportunity of investing in another fund and the expected upside is significantly higher than tax paid,” he explains.

Bala insists that it is incorrect to conflate every PMS with high churn, which is a legitimate concern for the traditional equity-based PMS. “Rebalancing within an MF portfolio is strategic and measured, not driven by stocklevel calls. The tax treatment at redemption of each MF unit applies, but it is no different from what an fund investor would suffer as tax.”

Execution unproven

MF-PMS makes a fervent pitch to solve a real gap in MF investing. Wealth managers position it as a vital tool for busy HNIs who have the capital but lack the time or emotional discipline to manage a complex MF portfolio themselves.

However, scepticism remains for this offering as it is yet to prove its credentials. Kumar emphasises that MF-PMS is best understood as the industry’s response to the July 2024 hike in short-term capital gains tax on equity, which made stock-level PMS churn uneconomical. “The wrapper is a regulatory adaptation by the provider, not a product improvement for investors. The investor’s problem, which was always cost and disclosure, has not been solved.”

Bala counters that outcomes will eventually prove the merit in MF-PMS. “Scepticism toward any new offering is natural, and doubly so when incumbents perceive it as a threat to their model. Distributors felt the same way when direct plans arrived. RIAs faced resistance when fee-only advisory was still a novel concept. In each case, the market eventually recognised the merit. MF-based PMS is at that same nascent stage.”

Ultimately, quality of advice will determine whether PMS-style advisory around MFs deserves its own place as a specialised, fee-based professional service.

{kind=link}