Real Economy: With moderation in inflation (both retail and wholesale), there is room for both fiscal expansion and monetary accommodation, supporting domestic demand and in turn industrial activities. The decline in wholesale prices will provide relief to corporates as they continue to face higher borrowing costs. Exporters will continue to face challenges as global trade remains subdued. Dun & Bradstreet expects the Index of Industrial Production (IIP) to have grown by 0.5% – 0.7% during April 2023, partly due to the base effect.

Price Scenario: Dun & Bradstreet expects inflation to moderate as global commodity prices continue to ease as the domestic supply side pressures ease and slower INR depreciation reduces imported inflation. However, the El Nino condition poses upside risks to our medium-term forecasts. Given the moderation in inflation, the Monetary Policy Committee (MPC) may opt for a prolonged pause in the interest rate cycle, unless the US FED pivots earlier. Dun & Bradstreet expects the Consumer Price Inflation (CPI) to be in the range of 4.1% – 4.3% and Wholesale Price Inflation (WPI) to be around (-) 2.6% – (-) 2.4% in May 2023.

Money & Finance: Dun & Bradstreet expects Indian G-sec yields to remain rangebound and largely unchanged in May 2023 compared to the previous month. Retail inflation print came below the Reserve Bank of India’s (RBI) upper tolerance limit for the second consecutive month raising hopes for the MPC to maintain status quo in the June policy meeting. We expect bank credit to continue strengthening, potentially reaching a multiyear high (~11 year) in the month of May 2023, an indication of sustained economic recovery. A survey conducted by Dun & Bradstreet supports this expectation that firms’ demand for short and long-term funds for Q2 2023 have touched 11-year and 2-year high, respectively. Dun & Bradstreet expects the 15-91-day Treasury Bills yield to remain at around 6.8%-6.9% and 10-year G-Sec yield to be 7.0%-7.2% for May 2023.

External Sector: Rupee is likely to remain under pressure in the month of May 2023. The Indian economy is exhibiting resilience to external headwinds and is expected to perform better compared to other emerging economies. The rate hike by the US Federal Reserve in May 2023 and concerns over the political standoff over US debt ceiling is supporting the dollar causing depreciation pressure on the rupee. However, the domestic currency may remain resilient in the medium term led by narrowing of current account deficit (CAD) and foreign capital inflows. Dun & Bradstreet expects the rupee to depreciate to 82.2 per US$ during May 2023.

Dr Arun Singh, Global Chief Economist, Dun & Bradstreet said, “In India, the softening of inflationary pressure is creating room for an extended pause in the policy interest rate. Despite the increase in lending rates, bank credit to the commercial sector is strengthening, current account deficit has eased, and inflation pressures have subsided, all of which point towards growing macroeconomic stability. It is however, pertinent to remain vigilant against potential risks from increase in crude oil prices, probability of El Nino conditions to create droughts along with increased global financial instability and unfavourable geopolitical developments”.

HealthCare Global Enterprises Limited (“HCG”), the leader in India in speciality healthcare services focused on oncology and fertility today announced its financial results for the quarter (“Q4”) and year ended FY23.

Highlights for quarter ended March 31st, 2023

Consolidated Income from Operations (“Revenue”) was INR 4,417 mn as compared to INR 3,639 mn in the corresponding quarter of the previous year, reflecting a year-on-year growth of 21.0%

Consolidated Profit Before Depreciation and Amortization, Finance Costs, Exceptional Items and Taxes (“EBITDA”) was INR 763 mn, as compared to INR 632 mn in the corresponding quarter of the previous year, a growth of 21% year-on-year

Consolidated Profit Before Other Income, Depreciation and Amortization, Finance Costs, Exceptional Items and Taxes (“Adjusted EBITDA”), was INR 831 mn, as compared to INR 676 mn in the corresponding quarter of the previous year, a growth of 23% year-on-year

EBITDA for Existing centers was INR 770 mn, a growth of 14% year-on-year

EBITDA from New centers was INR 83 mn, as compared to INR 37 mn in the corresponding quarter of the previous year, a growth of 122%

Consolidated Profit after Taxes and Minority Interest (“PAT”) was a profit of INR 84 mn, as compared to INR 60 mn in the corresponding quarter of the previous year, a growth of 40%

INR million except earnings per share

Period ended Mar’23

Q4-FY23

Q4-FY22

Growth

(y-o-y)

Income from Operations

4,417

3,646

21%

EBITDA(1)

763

632

21%

EBITDA margin (%)

17.3%

17.3%

Adjusted EBITDA (2)

831

676

23%

Ad. EBITDA margin (%)

18.8%

18.5%

PBT (3)

131

9

1355%

PBT margin %

3.0%

0.3%

PAT (4)

84

60

40%

PAT margin %

1.9%

1.6%

Earnings per share (EPS)

0.60

0.54

–

(1) Profit before depreciation and amortization, finance costs, exceptional items and taxes

(2) EBITDA excluding other income

(3) Profit / (Loss) before tax and after share of profit / (loss) of equity accounted investee, exceptional items

(4) Profit / (Loss) for the period after share of profit / (loss) of equity accounted investee, taxes and minority interests, exceptional items

Business Updates for Q4 FY24

HCG Emerging centers continued their scale-up trajectory:

o Strong revenue growth of 32% y-o-y

o Recorded strong EBITDA growth of 122% y-o-y

Several regions delivered double-digit revenue growth on sequential:

o Kolkata upsurge continued across all centers and delivered 142% revenue growth y-o-y

o Rajkot witnessed a continuance in its growth path with 58% revenue growth y-o-y

o Ranchi recorded a high growth of 51% y-o-y

Other highlights

o Total AOR for Q4FY23 increased to 65.1% in Q4FY23 compared to 59.9% in Q4FY22

o Emerging centers AOR saw a growth from 65.7% AOR in Q4 FY23 from 52.9% in Q4 FY2

Commenting on the results, Dr. B.S. Ajaikumar, Executive Chairman, HealthCare Global Enterprises Ltd.

said, “HCG being a single specialty hospital network, we have clearly shown how high-quality cancer centres can be established in a country like India, and how well it can perform in terms of clinical outcome and quality of care, at the same time grow financially, in the right way. For me as an Oncologist, and as a founder, it has been satisfying to see how HCG has become a medical destination, today.

Given the quality of our innovation, research, and patient-centricity, HCG ensures access to world-class cancer treatments and services for our patients. At HCG, we actively participate in clinical trials and invest in groundbreaking research to advance the frontiers of cancer treatment. Our Tumor board initiative is a potent platform that brings together a multidisciplinary team of oncology experts to discuss complex cancer cases, share insights, and develop personalized treatment plans. Employing breakthrough technology including Advanced Adaptive AI, Robotics, and Genomics coupled with our pay-per use model for LINACs enables us to provide best-in-class treatment at cost effective prices.

Our relentless fight against cancer is founded on our continuous research and technological innovation towards exploring new therapeutic avenues to move up the value chain of clinical excellence and lasting outcomes.”

Mr. Raj Gore, CEO HealthCare Global Enterprises Ltd., added, “We are extremely happy to announce our stellar performance for FY23. We have been consistently outperforming the industry growth with revenues for FY23 growing by more than 21% on a Y-o-Y basis. Our efforts on operational efficiency coupled with operating leverage has resulted into adjusted EBITDA growth of 31% leading to 139 bps margin expansion which stands at 18.9% in FY23, compared to 17.6% in the previous year.

Our track record of consistent performance reflected in highest ever revenue and EBITDA for 9 and 8 quarters respectively, in a row, is a testimony of meticulous planning and rigor in execution, we have shown as a team.

In addition to driving higher utilization of existing capacity, we would continue to invest in superior clinical expertise, capacity creation and brand building, to fuel future growth, and further fortify our leadership in the industry.

HCG remains to be the trusted healthcare partner for every individual, battling cancer. We are honored to have earned the trust of our patients and the communities we serve, and are committed to upholding that trust every day. Through our relentless endeavor we assure our patients the best of the treatments available across the globe and live up to our promise “Adding Life to Years”

Cosmo First Limited today declared its financial results for the quarter ended March 2023.

During the quarter, commodity films margins in both BOPP and BOPET suffered a further decline severely impairing the profitability of the industry. Cosmo with over two third of its revenue coming from speciality films could withstand the margin pressure and outperformed the industry once again.

The company expects the position to improve in the coming months bringing an end to QoQ declining phase, happening since the last 3 quarters. The company will continue to build its speciality products portfolio and maintain its lead over the other industry players.

The company’s pet care vertical continues to grow rapidly and clocked monthly run rate revenue (GMV) of Rs. 2 crores from its 15 experience centres and increasing online presence through its website and mobile app. An acquisition opportunity in the online pet care space is in the final stage and is expected to be closed soon. This would further accelerate the growth of the pet care vertical.

The speciality chemical subsidiary is set to launch newer adhesives which together with healthy growth in the masterbatch vertical would enable the subsidiary to have further growth in FY 23-24.

The company’s balance sheet remains strong with substantial cash reserve and net debt to EBITDA of about one time.

The Board of Directors had recommended a dividend of Rs 5 per equity share for the financial year FY 22-23 subject to approval of shareholders in the annual general meeting. This coupled with the 1:2 bonus in June 2022 and share buyback with tax-free handsome gain over the market price in February 2023 affirms the company’s commitment to provide regular returns and share prosperity with the shareholders.

Commenting on company’s performance Mr. Pankaj Poddar, Group CEO, Cosmo First Ltd. said “The company has launched many new specialty films including shrink for packaging and non- packaging applications. Several other speciality films for non-packaging applications are in the pipeline and should hit the market in coming quarters. All these would further strengthen the company’s position in speciality films business.”

Tata Hitachi, a leading provider of Construction and Mining Equipment, announced its First Edition of Annual Financiers’ Summit and Awards Show – Synergie 2023 at ITC Maratha, Mumbai.

Synergie 2023 – a Summit and Award ShowforFinanciers – gives Tata Hitachi a forum to thank Finance Partners and recognize their efforts by rewarding top performers. It also providesa unique platform to engage and co-create better financial solutions for our esteemed customers.

Speaking on the occasion, Mr Sandeep Singh, Managing Director Tata Hitachi said, “It gives me great pleasure to host Synergie 2023 – the First of an Annual Summit to felicitate our Finance Partners. Financiers are an important stakeholder in our Construction Equipment ecosystem.

We believe that this summit will help further strengthen our relationship with our Finance Partners and help us to continue to grow and innovate.”

Cosmo Ferrites Limited, a leading manufacturer and exporter of Soft Ferrites and an emerging player in wire wound magnetic components today declared its financial results for the quarter ended March 2023.

Enhanced Q4 results vs. Q3 is mainly on the back of some normalization of order flows from Europe which was impacted due to over stocking/recession fears/chip shortages.

The new kiln for valued added speciality cores has been commissioned at Q4 end FY 22-23 and should add to revenue/profitability in the coming quarters.

Q4 results included Rs. 80 lakhs charge under ‘other expenses’ on account of loss on sale of an old asset. There was also an ‘other income’ of Rs 91 lakhs towards interest and legal expenses recoverable pursuant to an arbitration award.

Commenting on Company’s performance Mr. Ambrish Jaipuria, Chairman, Cosmo Ferrites Ltd. said “The Company is working on several medium-term growth prospects particularly in automotive sector and expect customer approvals in FY 23-24 which should lead to margin expansion.”

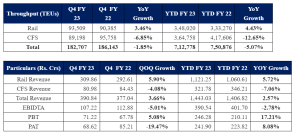

Gateway Distriparks Limited (GDL), a leading integrated inter-modal logistics facilitator in India, today announced its audited financial results for the March quarter of the current financial year.

Note: The Company was operating CFS Punjab Conware in Nhava Sheva for 10 months in FY22 after which the O&M agreement expired. Punjab Conware FY22 revenue was Rs. 87.52 crores and EBTIDA was Rs. 15.84 crores. However, after payment of license fees Rs. 16.44 crores to Punjab State Warehousing Corporation, it was a loss making facility for the company. For a like-to-like comparison, excluding Punjab Conware CFS from the Company’s throughput and financials, on a YoY basis, the total throughput grew by 6.91% , total revenue grew by 10.5% and total EBITDA grew by 1.2% for the full financial year.

Prem Kishan Gupta, Chairman and Managing Director, commented,“We are pleased to report healthy financial performance for the company for the quarter and year ending 31st March 2023. While there has been a slowdown in Export volumes in the past six months, signs of recovery are now being seen from April onwards. Import volumes have been growing to a large extent. Our focus remains on improving efficiencies and expanding our network. In the beginning of FY23, we had allocated Rs. 500 crores towards capital expenditure to be utilised by fiscal year 2025, with about Rs. 200 crores already invested thus far towards the acquisition of ICD Kashipur and land procurement and initial development of ICD Jaipur. Our goal is to invest the remaining amount in new projects and we are actively exploring both greenfield and acquisition options in Northern and Central India to expand our network of ICDs in the next two years.”